We aren’t breaking news to tell you that the language of taxes is remarkably obscure. There are tax code numbers, endless terms, numerous IRS tests, and so much more, which all become extremely important on Tax Day.

You’re not an accountant, but for founders, CFOs, and CEOs, understanding the language of taxes can help you strategize from a position of strength. So, we’re proud to present “The Language of R&D Taxes, Translated”, a helpful cheat sheet from your friends at Neo.Tax :)

Tax Lingo

Capitalization - capitalization can be understood as a limitation on the timing in which you can take a deduction. There are two different subgroups of capitalization: depreciation (for physical assets) and amortization (for intangible assets).

Deduction - a deduction can be thought of as an expense that is subtracted from taxable income. So, if you made $10 mil in revenue and spent $5 mil on R&D, deducting that amount would make your taxable income $5 mil ($10,000,000 minus $5,000,000).

Doing Business As (DBA) - a DBA is a name other than one’s legal name that a person or company does business under.

Employee Identification Number (EIN) - a nine-digit number assigned by the IRS, used to identify taxpayers who are required to file various business tax returns.

NOL - a Net Operating Loss means how much in the red you are in a given tax year. So, if your startup is pre-revenue or early-revenue, every dollar you spend on payroll, marketing, R&D, or rent over the amount brought in via sales would be counted as an NOL.

Unused NOL - if the loss is not fully used up in the carryback years, any unused portion of the loss may be carried forward for up to 20 years after the NOL year. Any NOL that is not used up in the carryover period is lost.

Taxable Income - the portion of your gross income that’s actually subject to taxation. Deductions are subtracted from gross income to arrive at your amount of taxable income.

Total Expenses - The cumulative sum of expenses from your accounting and payroll systems.

R&D-Specific Lingo

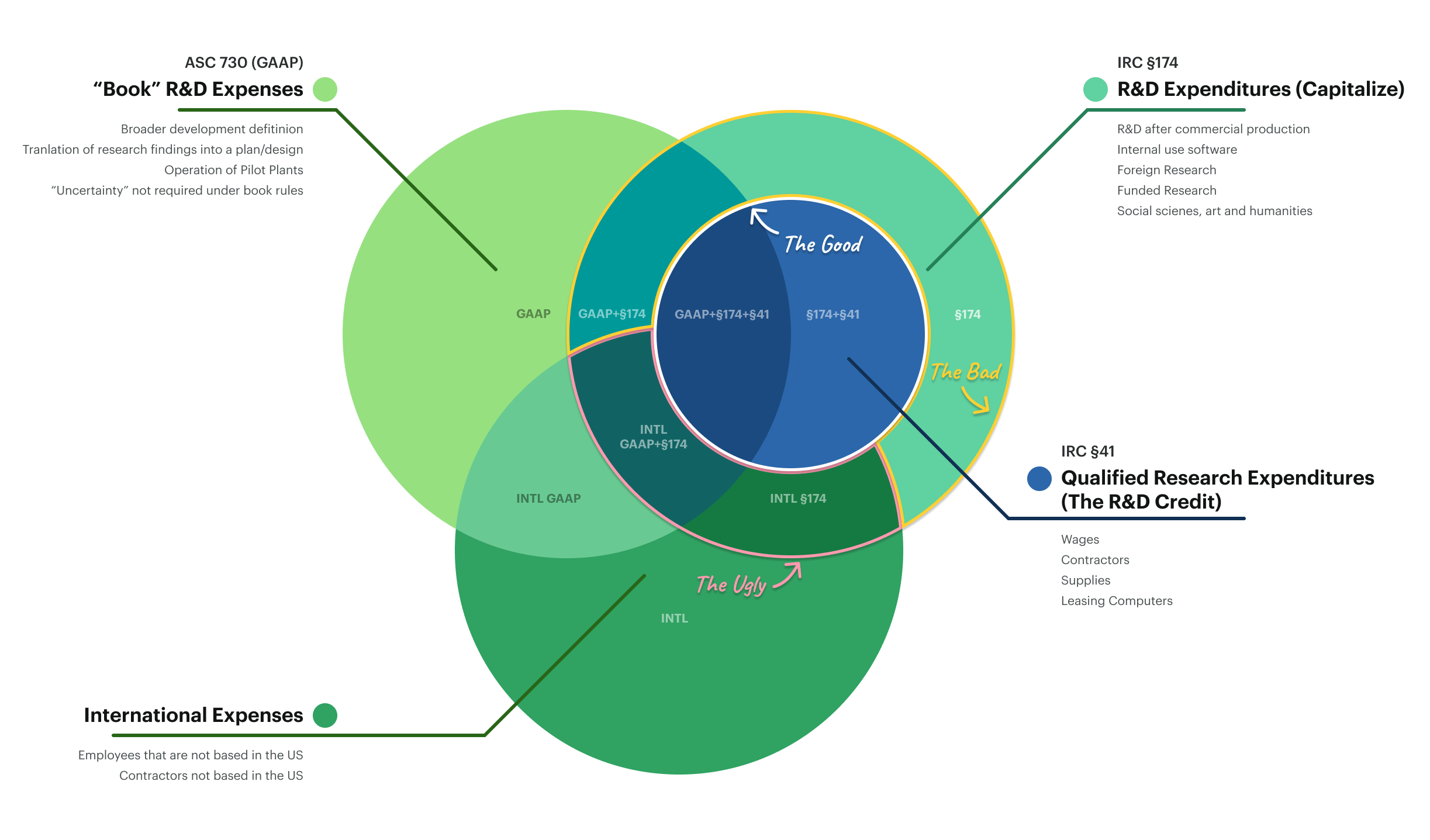

**R&D Credit ****- **enacted in 1981 to encourage research and development (R&D) activities in the United States, the R&D tax credit reduces tax liability for organizations that perform certain activities to develop new or improved products, processes, software, techniques, formulas, or inventions. You can get about 10% back on qualifying expenses such as wages, contractor costs, cloud hosting and infrastructure, supplies, and legal costs.

Expenses allocated to R&D - direct expenditures relating to a company’s efforts to develop, design, and enhance its products, services, technologies, or processes.

Qualified Expenses - these are the expenses covered by IRC Section 41. They are the expenses eligible to be claimed as part of the R&D Tax Credit (they must pass the IRS’s 4-Part Test to qualify), such as:

- W-2 Employees (W2, Box 1 Wages) - all taxable wages including bonuses and stock-option redemptions

- Payments to contractors

- Cloud hosting and infrastructure

- Patents

- Cost of Supplies

**The 4-Part Test **- for an R&D expense to qualify for the R&D Tax Credit, it must pass the IRS’ 4-Part Test. It must:

- work to eliminate a technical uncertainty.

- experiment via modeling, trial-and-error, simulation or other methods.

- use an experimentation process relies on a hard science.

- have the goal to create a new or improved product or system.

New or improved business component (product/process) - the first part of the 4-Part Test: The research must be focused on developing a new or improved business component for the company. A “business component” means any product, process, computer software, technique, formula, or invention held for sale, lease, or license or used in a trade or business. This can include improving the function, performance, reliability, or quality of an existing product or business component.

Technological in nature - the second part of the 4-Part Test: The research relies on principles of the physical or biological sciences, engineering, or computer science, including software development.

Attempts to eliminate uncertainty - the third part of the 4-Part Test: The research aims to eliminate uncertainty concerning the development or improvement of a business component. For example, the method or appropriate design is not apparent and not readily found in the public domain. Essentially, an uncertainty can be “How can we develop this new application?” or “Could this material make our product lighter without sacrificing durability?”

Process of experimentation - _the fourth part of the 4-Part Test: _The research must be a process of evaluation and generally should involve comparing alternatives looking for the best solution. This includes the iterative trial and error process inherent in version-controlled software development.

Non-qualified R&D (IRC Section 174) - these are R&D expenditures that DO NOT qualify for the R&D credit:

- R&D after Commercial production

- Internal use software

- Foreign Research

- Funded Research

- Social sciences, art, humanities

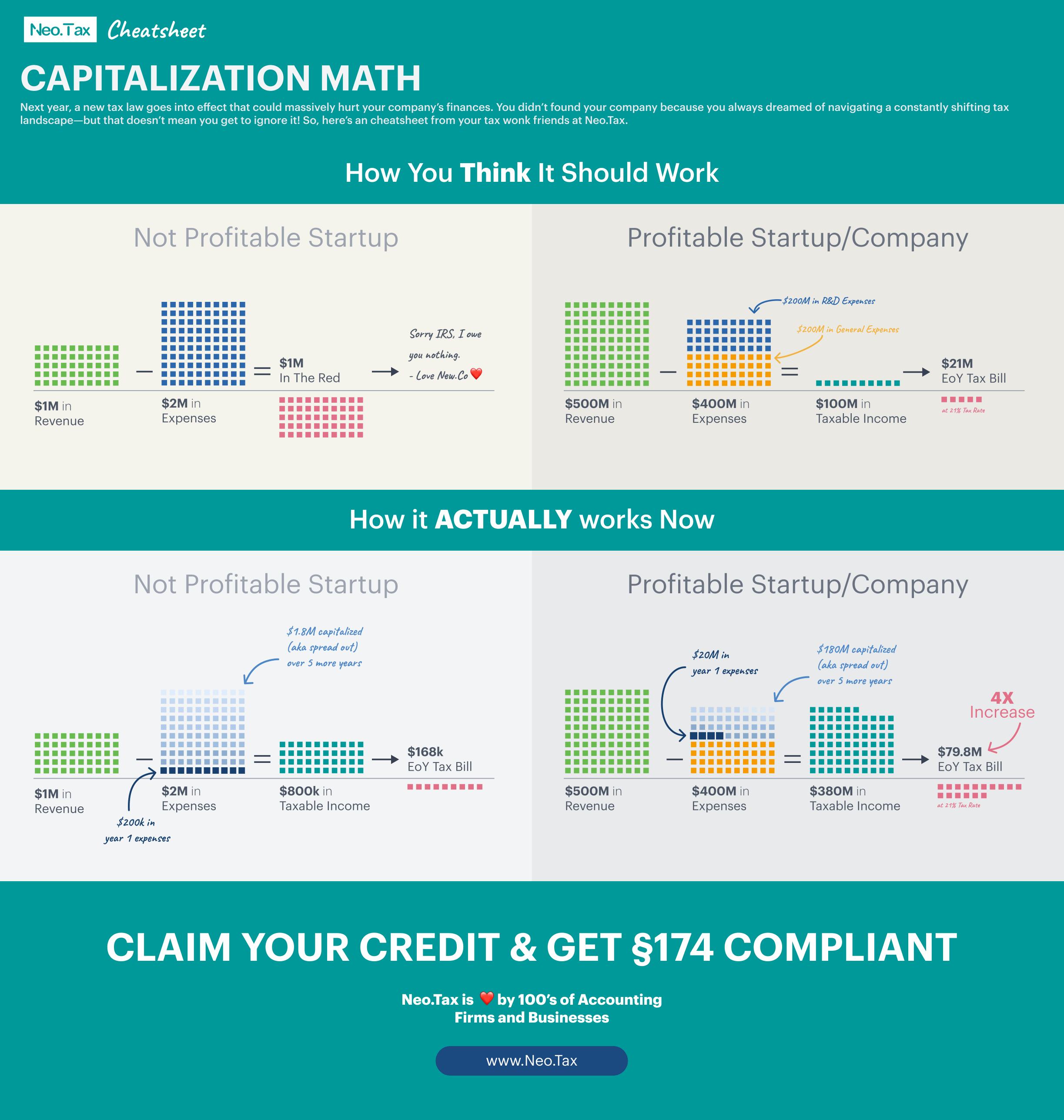

Deductible R&D - In years prior, companies were permitted to deduct R&D expenses in the year they were incurred. Beginning in tax year 2022, that is no longer the case. Instead, you are now required to amortize those expenses over five for domestic R&D or 15 years for foreign R&D.

Foreign R&D - R&D performed abroad by U.S.-located companies.

R&D Capitalization - as part of the TCJA, you can now only deduct a fraction of total R&D expenses. That means companies may now find that they have a taxable income, even through they are not yet profitable. The graphics below highlight this point:

Before these changes were written into law, 100% of your R&D spend could be deducted from your income. If you brought in $1M in revenue and spent $2M on R&D to develop your innovative product, you would end the year with $1M in Net Operating Losses (NOLs). Now, you have to spread the R&D deduction over 5 or 15 years depending on if the spend is made in the United States or abroad—this is called amortization. Worse than that, only 6 months of the first year of R&D spend can be deducted. So, if the $2M you spent on R&D is domestic, you’ll only have $200K to deduct from your $1M.