Even though R&D Capitalization was passed into law back in 2017 as a part of Former President Donald Trump’s Tax Cuts and Jobs Act (TCJA), almost everyone expected the massive tax law change to be repealed before it ever took effect. But for the last year-plus, we’ve been preparing for the possibility — which has become a reality — that R&D Capitalization is here to stay (at least for now).

Since September, we’ve written a collection of articles explaining The What, The Why, and The How-the-Heck-Do-I-Keep-My-Tax-Bill-Low of R&D Capitalization. We’ve also spent the year building the only software solution that solves for both R&D Tax Credit Filing and R&D Capitalization. So, book a call and we can talk you through any specific strategy questions.

Without further ado, Neo.Tax presents: Your Definitive Guide to R&D Capitalization…

What is R&D capitalization?

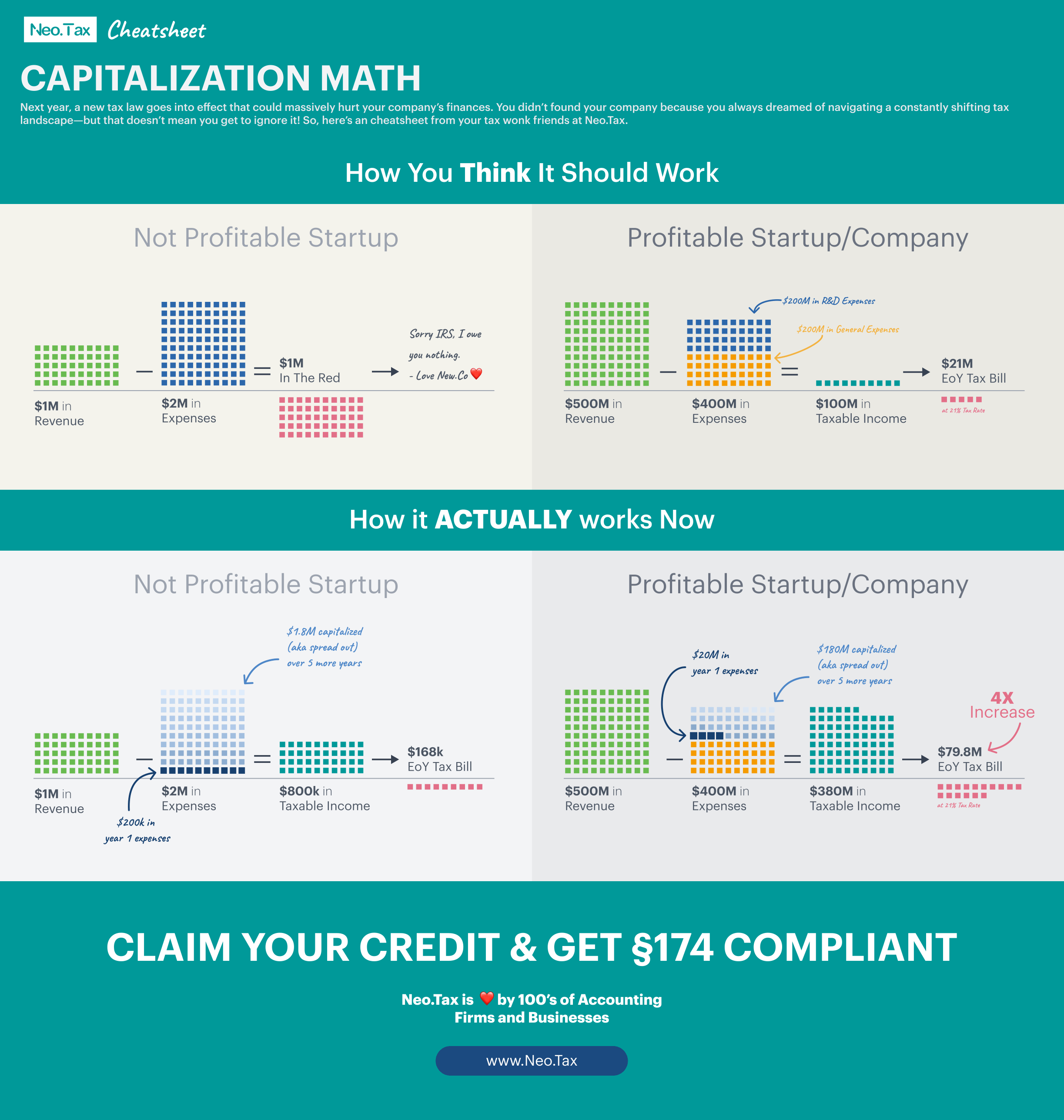

The TCJA changed the way that R&D expenses can be deducted by American companies. Up until this Tax Year, R&D could be deducted all at once, meaning that innovative companies who spent on R&D would appear in the red both in their books and in the eyes of the IRS. However, the new law states that R&D expenses must be amortized over 5 or 15 years (depending on if the expenses are domestic or international). Therefore, only a fraction of a company’s R&D expenses can now be deducted in a given year.

All of a sudden, pre-revenue startups will begin to appear in the black in the eyes of the IRS — so what would have been a valuable NOL will now be a hefty tax bill. And startups are not the only ones affected: CFOs from the largest American companies have warned Congress that this change will stifle innovation. Yelp’s effective tax rate will jump 20 percent this year compared to 2019 due to R&D Capitalization!

Do we have to capitalize?

We’ve heard from many companies who are confused by the change. They ask: if we don’t file an R&D credit, do we still have to capitalize our R&D expenses? The short answer is YES. An accountant is responsible for making sure your filing is compliant with the law. R&D Capitalization is the law (at least for now). So, not amortizing your R&D expenses is not an option. In the event of an audit, the IRS may be inclined to disallow any R&D credit and/or re-calculate the expenses claimed.

So, as of now, any expense that can be categorized as an R&D expense must be amortized over 5 or 15 years whether or not you file for the R&D credit. Therefore, companies that forgo the money they’re owed in the form of a credit will simply be burdened with an even higher tax bill this year.

The true effect of the change is that it makes it imperative for innovative companies to commit to Tax Strategy year-round to minimize the impact on their tax bill. R&D expenditures that are considered “qualified expenses” can be claimed on an R&D credit; those that are not “qualified” now must be amortized. The difference between qualified and not qualified R&D spend come Tax Day? Almost 10x.

What is a qualified vs. non-qualified research expense?

Okay, so, clearly it’s essential to maximize “qualified” expenses and minimize “non-qualified” R&D costs. But what is the difference between the two?

IRC §41 (Section 41) defined a “qualified” expense that can be claimed via the R&D Tax Credit as any R&D expense that passes the Four-Part Test: Permitted Purpose; Elimination of Uncertainty; Process of Experimentation; Technological in Nature. You can read more about the Four-Part Test here, but basically, these are expenses directly related to the creation of new products or novel uses of existing products (that includes wages, research expenses, supplies, and even cloud computing costs).

Now, IRC §174 (Section 174) defines the way companies must deal with all R&D expenses: both “qualified” and “non-qualified”. But obviously, the larger the percentage of your R&D spend that “qualifies” for an R&D credit, the smaller the amount that you’ll need to amortize. Examples of R&D costs that are not qualified (aka do not pass The Four-Part Test) include: R&D after commercial production; research for internal use only; research funded by a grant; and most research tied to social sciences, arts, and humanities.

To be an innovative company, R&D spend is essential. So, the key now is maximizing the percentage of that spend that qualifies for an R&D credit and minimizing the spend that must be amortized over 5 or 15 years.

Why do we have to include foreign expenses?

As long as you’re a company doing business in the United States, you have to pay taxes in the United States. In many ways, the reason for this massive change to R&D taxes is an effort to move more research jobs and spending back into the United States.

The amortization structure is designed to punish R&D spend made outside of American borders. A quick example to explain why the 15-year amortization is so much more punitive than the 5-year amortization:

In its simplest form, a deduction can be thought of as an expense that is subtracted from taxable income. So, if you made $10M in revenue and spent $5M on R&D, deducting that amount would make your taxable income $5M ($10,000,000 minus $5,000,000). But under the new R&D capitalization rules, the amendment means the deduction must be amortized, or in simpler terms, spread over 5 or 15 years, depending if the expense is domestic or international, respectively. On top of that, Year 1 can only be amortized as half a year, so that means only one-tenth or one-thirtieth of the R&D expenses can be subtracted from the taxable income that first year.

So, if your company’s R&D occurred in the States, the equation becomes $10 mil minus $1M; if it’s done abroad, the equation becomes $10M minus $333,333.33. Eventually, over the 5 or 15 years, you will technically be able to deduct the same amount as before, but this obviously increases your tax bill in the near term by quite a bit. For the company that spent exclusively in the States — that’s a $9M taxable income; for the company that did R&D abroad, that’s $9.67M. With the 21% corporate tax rate, for Year 1 taxes, that’s an extra $140K!

Will capitalization be repealed?

This is the big question, and for now, the only responsible answer is: NOT YET.

For the last six months, there have been rumors that a deal is close, but none have come to fruition. Many CEOs, CFOs, and even accountants are keeping their fingers crossed, but, unfortunately, the Crossed Fingers Method is not IRS-compliant.

So, the safest route forward is to either file now and hope the law is repealed and companies are retroactively made whole for their 2022 or to file an extension, pay your quarterly taxes as if the law is still on the books, and then hope that your quarterly taxes are refunded if the law is eventually overturned. Either way, make sure to file an R&D credit when you file your taxes — they cannot be filed retroactively.

As anyone who has watched Washington these last five years knows: betting on compromise is a longshot wager. So, plan as if the law on the books is the law of the land, and get your books in order. And, remember: we’re here to help! So, book a call today.

The Takeaway

If you’re a company involved in software, manufacturing, architecture, engineering, food, or construction, it’s very likely that you qualify for an R&D credit. It’s just as likely that you have expenditures that can be considered R&D spend.

Two things to remember…

- Any company with R&D expenditures needs to amortize their deduction to be compliant with the new R&D Capitalization rules.

- The best way to offset that cost and extend runway in a non-dilutive way is to claim your R&D credit. It’s the closest thing to free cash for innovative companies. It’s written specifically for companies like yours. So, don’t leave that money on the table!

Neo.Tax is the only software solution that solves for both R&D Capitalization and for R&D credit filing. Let us help you navigate this massive change. We’ve been deep in the weeds on this for 12 months; we’d love to walk you through the best way to maximize your credit and minimize the impact of capitalization!