Since September 2022, we’ve been banging the drum about Section 174 and how it punished U.S. companies who invested in R&D. Well, with its passage last week, the Trump administration’s One Big Beautiful Bill has dramatically altered the corporate tax landscape.

How We Got Here

As we explained then, in 2017, when President Donald Trump signed into law his landmark Tax Cuts and Jobs Act (TCJA), the Congressional Budget Office—tasked with nonpartisan analysis of the TCJA—found that the new tax code would vastly increase the national deficit between 2018 and 2028. The main reason was a new single corporate tax rate of 21% (down from 35%). In an effort to recoup some of those lost taxes, Congress modified the TCJA to include a massive change to the way R&D expenses are treated, which went into effect in the tax year 2022.

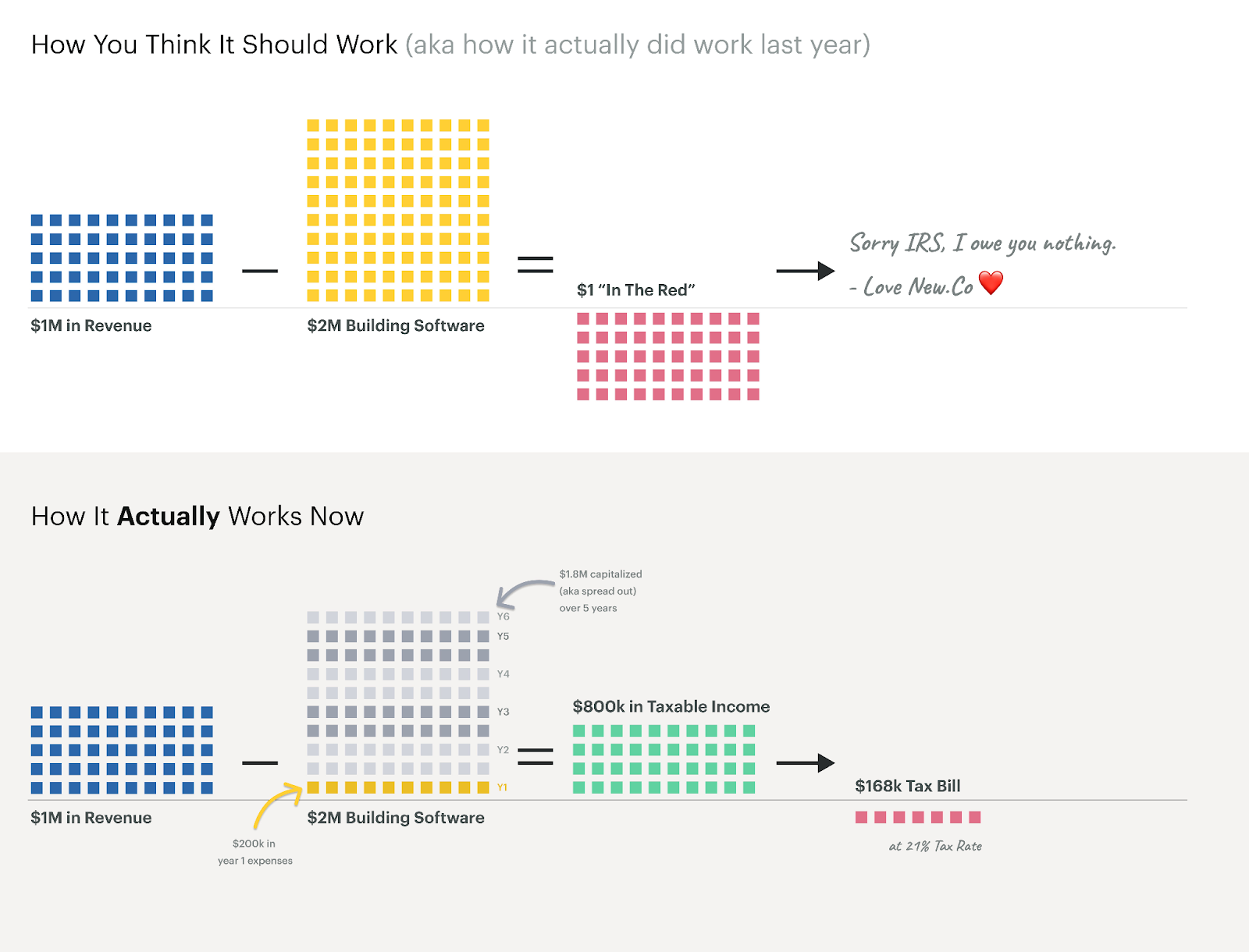

The change, which forced innovative companies to amortize rather than deduct their R&D spend, cost U.S. businesses dearly. Basically, by dividing domestic deductions over a 5-year period, companies could no longer count qualified R&D expenses against their revenue. That meant they were hit with burdensome tax bills, far outstripping the amounts they had planned for

Back in 2022, we shared this graphic, which illustrated the impact:

The New Reality

Now that you understand the landscape and how we got here, here’s the massive change that just occurred. On July 3rd, the House passed the budget bill President Trump has dubbed the “One Big Beautiful Bill Act”. Tucked within the OBBBA (Section 70302) is a massive boon for U.S. corporations. While it’s not a full reinstatement of the old way of expensing R&D, the OBBBA dramatically improves the playing field.

For our purposes, the key details are:

- While international R&D expenses will still need to be amortized over 15 years, domestic R&D expenses can once again be deducted from current year revenues, starting in the 2025 tax year.

- Companies that had begun capitalizing domestic R&D expenses from 2022 to 2024 can now elect a Catch-Up Deduction, in which they deduct all the remaining unamortized R&D expenses in a single year. This deduction can be made in the 2025 tax year, and can significantly improve cash flow by lowering their tax burden.

- Eligible small businesses may choose to retroactively apply a full expensing of their R&D to all tax years beginning with 2022, which will allow them to amend prior returns and recover amortized costs they’d already spent.

What This Means for You

The mechanics of how to maximize your R&D credit is complicated, but the tax experts at Neo.Tax can walk you through the process and help you take advantage of this unprecedented opportunity.

Many in Silicon Valley had been loudly calling for Section 174 to be changed back to its pre-TCJA form. After plenty of deadlock in Congress these last few years, it’s finally happened. So it’s more important than ever to understand the best way to be strategic when it comes to R&D.