What is the R&D Tax Credit?

The research and development (R&D) tax credit is tax legislation passed to incentivize American companies to invest in innovation.More than $12 billion worth of R&D tax credits were claimed in 2014, but a significant portion 0of that money went to Fortune 500 companies. Congress has taken specific action of the last half-decade to make sure the credit is available to early-stage startups. The goal is to give innovative startups the tax credit they need to create new, valuable ideas in the United States.

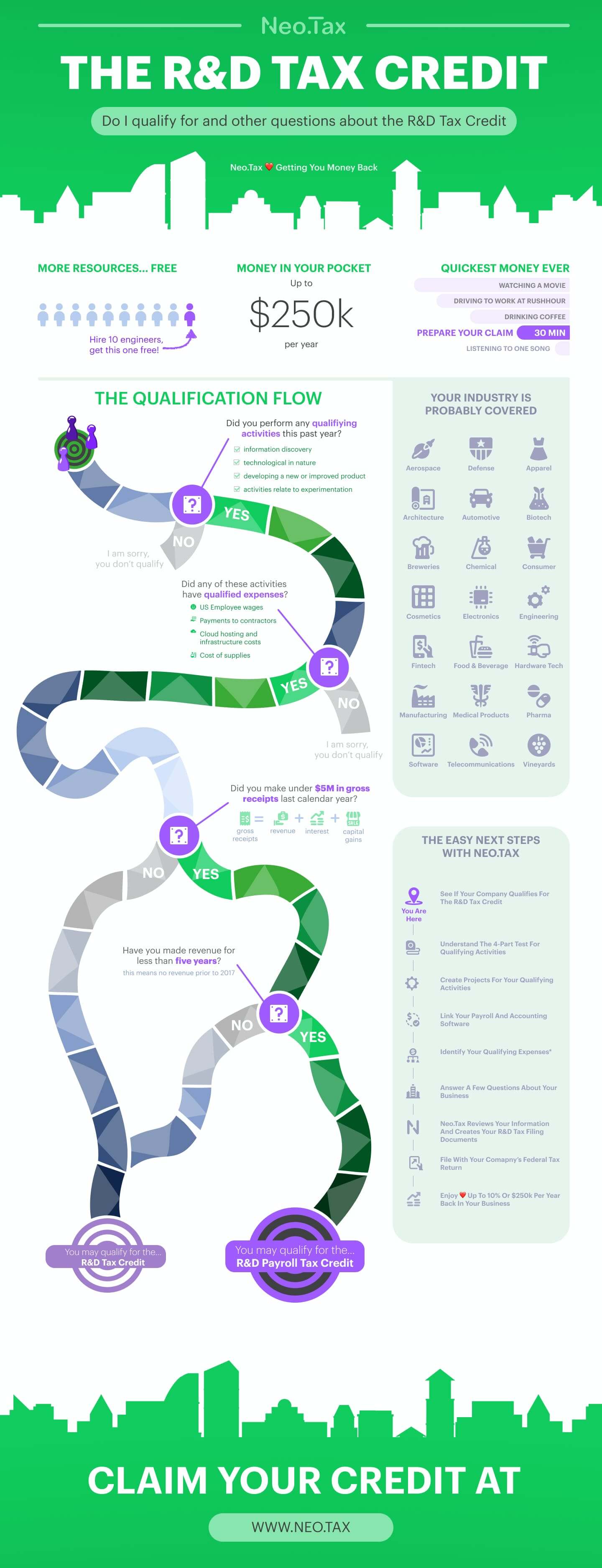

Does my startup qualify for the R&D Tax Credit?

If you’re a startup in the tech space, you more than likely qualify for the R&D Tax Credit. The qualifications for the credit are:

- You are working to eliminate a technical uncertainty.

- You are experimenting via modeling, trial-and-error, simulation or other methods.

- The experimentation process relies on a hard science.

- The goal of this process is to create a new or improved product or system.

Importantly, in order to use the R&D Credit towards your payroll rather than your income, you must also fit these 3 criteria:

- Less than $5 million in revenue.

- Less than 5 years since first revenue.

- Employees (and payroll taxes) in the U.S.

How much can the R&D Tax Credit save my startup?

The 2016 expansion of the R&D Tax Credit allows startups to claim the credit against their payroll tax for up to 5 years. Each year, they can receive a maximum credit of $250,000, so theoretically, a company could receive a maximum of $1.25 million over their first five years.

Why haven’t I heard of the R&D Tax Credit before?

First, the tax code is purposely obscured. Second, the R&D Tax Credit didn’t apply to startups like yours until 2016. The newness of the law means many companies are leaving money on the table. But, we’re here to help. neo.tax’s automated filing system can complete the process for your company in less than 15 minutes. We take just 5% of your savings and only after they arrive in your bank account. The R&D Tax Credit was written for startups like yours; get the money that you’re owed.

History of the Tax Credit

When Ronald Reagan signed the Economic Recovery Tax Act of 1981 into law, businesses quickly jumped to take advantage of the new tax break that let them lease or rent computers. At the time, computers were prohibitively expensive, which made them impossible to own for all but the largest corporations and research institutions. Instead, most people leased time on mainframe computers. The 1981 bill made it so the money companies spent leasing mainframe computers were Qualified Expenses towards a tax credit. While the bill was built to democratize access to computers in the business world, it ended up becoming most valuable for the largest companies. In a section of The Protecting Americans From Tax Hikes Act of 2015 (PATH), congress set out to fix that issue. For years, the R&D tax credit could only be used to offset a company’s income tax. Obviously, most early-stage startups don’t have any income to offset. So, starting in 2016, in order to incentivize innovation at the early startup level, the PATH Act allowed early startups to use the R&D Tax Credit towards payroll tax as well. That law made thousands of startups newly eligible for the R&D Tax Credit; unfortunately, most still don’t realize or have the resources to file for the money they’re owed.